Introduction

In project finance, the Loan Life Cover Ratio (“LLCR”) is an important metric for lenders, alongside other key ratios such as the Debt Service Cover Ratio (“DSCR”). The LLCR assesses the ratio of the Net Present Value (“NPV”) of future Cash Available for Debt Service (“CFADS”) to the outstanding Debt Balance. Unlike the DSCR, which evaluates a project’s ability to service its debt within a single period, the LLCR measures a project’s capacity to fully repay outstanding debt based on anticipated future CFADS. The higher the LLCR the greater a project’s ability to repay outstanding debt.

When arranging debt (pre ‘financial close’)

Similar to the DSCR, lenders typically require the financial model to demonstrate a minimum LLCR is being met as a ‘Condition Precedent’ (“CP”) to signing the financing agreement / initial drawdown of funds. An average LLCR is not typically mandated as a CP, unlike the DSCR, as it is a measure that already inherently considers the full debt term.

However, whilst the DSCR – whether minimum or average – is often the key constraint that dictates the total quantum of debt that can be drawn, or the minimum annual payment required from the Grantor in a Public Private Partnership (“PPP”) tender process, the outturn LLCR is less likely to be the constraining factor.

Once debt has been invested (post ‘financial close’)

As with the DSCR, the LLCR will also be monitored at regular intervals once senior lenders have invested their capital. Again, where the LLCR falls below agreed-upon thresholds, the project may enter ‘lockup’, with equity distributions prohibited or, more drastically, ‘default’, where lenders can assume control of the asset to safeguard their investment. As the calculation of the LLCR will ordinarily result in a higher value than the DSCR in the base case (see Figure 1 below), lockup and default thresholds included in the financing documentation should also be correspondingly higher.

It is important to note that as the LLCR is a forward-looking metric spanning the entire debt term it is sensitive to the technical and economic assumptions used to derive CFADS. These assumptions may be mandated by the ‘agent bank’, making them a potential source of contention where they result in lockup or default. In contrast, whilst a forward-looking DSCR is also calculated this will generally only cover the following 12-month period, with the assumptions underpinning this less likely therefore to be a point of disagreement.

The LLCR is a forward-looking ratio that tests a project’s ability to repay the outstanding debt balance given the anticipated CFADS generated over the remaining debt tenor. It is tested on each debt repayment date, usually quarterly or semi-annually, calculated as follows:

Each of the three components of the LLCR are discussed below, noting that the detail of the financing documentation should always be checked when calculating ratios as the theory and practical reality do not always align.

1. Net Present Value of future CFADS

The two principal questions to answer when calculating the NPV of CFADS are:

- What discount rate should be used?

- What cash flows should be included in CFADS?

Discount Rate

As already noted, the LLCR is a measure of a project’s ability to repay outstanding debt given future anticipated CFADS. Therefore, to determine whether future CFADS is sufficient to repay the debt balance we must discount this by the rate it would grow at over time, i.e. the interest rate. In simple terms, if 100 of debt is outstanding with interest accruing at 5% per annum, CFADS of 105 will be required in one year’s time to repay the debt balance. If we assume only one year of cash flows remain then discounting CFADS of 105 with a 5% discount rate equals 100, resulting in an LLCR of 1.00x.

The financing agreement will specify the discount rate to be used which can be broadly expected to be defined as the “weighted average interest rate applicable to the senior facilities in each calculation period” (perhaps within a wider definition of ‘Discounted Available Cashflow’ or ‘Net Present Value’). To the extent therefore the interest rate fluctuates over time, for example due to a stepped margin, it will be necessary to create a manual discount index for modelling purposes, rather than discounting CFADS using Excel’s inbuilt XNPV function.

What cash flows should be included in CFADS?

Firstly, as the LLCR tests the ability of a project’s future cash flows to repay outstanding debt, only CFADS generated after the date the ratio is being tested for should be included. For example, if the denominator uses the debt balance from 31/12/2025 the numerator should discount CFADS from 1/1/2026 onwards.

Furthermore, as the LLCR is a Loan Life Cover Ratio, only CFADS generated within the debt tenor is relevant – otherwise a Project Life Cover Ratio (“PLCR”) will be calculated, where CFADS generated to project expiry is considered (i.e. including the period between debt maturity and the end of a project).

Regarding the makeup of CFADS, this may already have been calculated for use in the DSCR, however there are a number of theoretical reasons however why it may not be correct to use the same definition, for example:

- Where the LLCR includes certain cash balances, such as the Maintenance Reserve Account (“MRA”), double counting can occur if CFADS also includes movements in and out of the reserve

- If the discount rate used in the LLCR reflects the full cost of servicing all facilities, e.g. potentially including commitment fees from a Debt Service Reserve Facility (“DSRF”), then CFADS shouldn’t also include commitment fees

2. Cash balances

The LLCR numerator often includes cash balances to the extent these would be available to repay outstanding debt. This may include any operating cash balances in addition to cash held in reserve accounts (such as the Debt Service Reserve Account (“DSRA”) and, potentially, the MRA).

As noted above, where reserve account balances are explicitly included in the numerator of the LLCR, the movements to/from these reserves should not also be included in CFADS – this represents double counting and will likely lead to an overstatement of the LLCR, reflecting the fact the NPV of reserve movements will usually be positive where reserves reduce to zero at debt maturity.

3. Outstanding debt

The LLCR denominator will most likely be the aggregate of all loans outstanding at the calculation date, capturing other facilities than can be drawn in addition to the term facility, such as a DSRF.

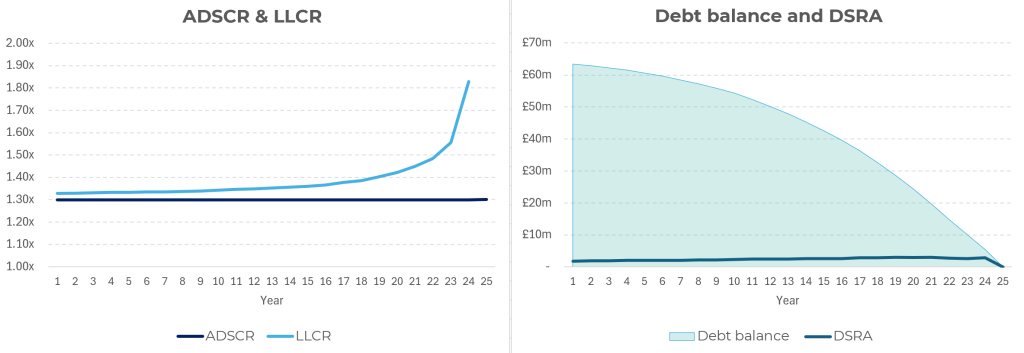

As you might expect the DSCR and LLCR are closely related, as both rely on similar underlying data, albeit with the DSCR being a single-period ratio whereas the LLCR is calculated using cash flows over the remaining life of the debt. Where the DSCR remains constant throughout the loan term and the same CFADS is used for the LLCR – without any cash balances included – the LLCR will be equal to the DSCR.

However, cash balances are typically included in the LLCR, resulting in a ratio that exceeds the DSCR. This difference usually widens over time, creating the upward sloping profile illustrated in Figure 1 below.

This occurs because the cash balances included generally remain relatively constant, whereas the debt balance declines over time, as can be seen in the chart on the right hand side, thereby increasing the ratio.

Figure 1: Relationship between ADSCR and LLCR

Evolution Infrastructure work with hundreds of third-party financial models each year across our modelling, audit and advisory service lines and we therefore encounter a variety of different errors when calculating the LLCR. A number these issues to look out for are highlighted below.

Double counting

As set out above, care needs to be taken to avoid potential double-counting in the following areas, noting that adherence to financing documentation definitions is paramount:

- CFADS discounted at the full cost of debt (e.g. including the cost of commitment fees within the rate) with the NPV of CFADS including commitment fees

- Inclusion of reserve balances in the LLCR numerator while the NPV of CFADS also incorporates reserve movements

Discount Rate with changing cost of debt

One of the most common errors we see relates to the use of a static discount rate, with no account taken of debt margins that may increase over time. A manual discount index should be created and periodic interest rates used – and whilst discounting CFADS by the Effective Interest Rate (“EIR”) on debt may capture increasing margins, over time it is not correct.

Mid-period discounting

Documentation also sometimes refers to ‘mid-period’ discounting, addressing the fact that cash flows (i.e. CFADS) may occur evenly through a modelling period rather than at the end (in contrast to debt service). This is sometimes incorrectly overlooked when calculating the LLCR, with the greatest impact occurring when model periodicity is longer, for example annual instead of quarterly periods.

Timing mismatches

Another common issue is a mismatch between the debt balance in the denominator and the cash flows in the numerator. This typically arises when the NPV of CFADS includes cash flows from a period that is either too early or too late—rather than starting from the day following the date on which the debt balance is being tested. As noted above, if the denominator uses the debt balance from 31/12/2025 the numerator should discount CFADS from 1/1/2026 onwards.

Missing debt balances

We occasionally see models that omit some of the debt facilities from the LLCR denominator, with this commonly occurring for facilities that aren’t drawn in the base case, for example a DSRF. Whilst this may have no impact in the base case is will lead to an overstatement in the LLCR in downside sensitivities.

Circularities

Finally, it’s important to note that because the LLCR is a forward-looking ratio, it can introduce a circularity when used as a trigger for a lock-up mechanism. Circularities should always be avoided in best practice modelling where possible. One way to address this is by hard-coding (or ‘pasting’) the LLCR results for use in the lock-up calculation. A common and generally accepted modelling simplification however is to not enforce the lock-up based on the LLCR within the model itself, but rather to flag and report when the LLCR falls below the threshold, indicating that a lock-up would apply in practice.

If you have found this article useful and would like further information about our training courses, then you can read more here.

To discuss your advisory, financial modelling or model audit requirements then speak to us about your project today by emailing us at info@evoinfra.com.